Some real estate loans reduce risk through complex structuring. Others reduce risk by starting with margin.

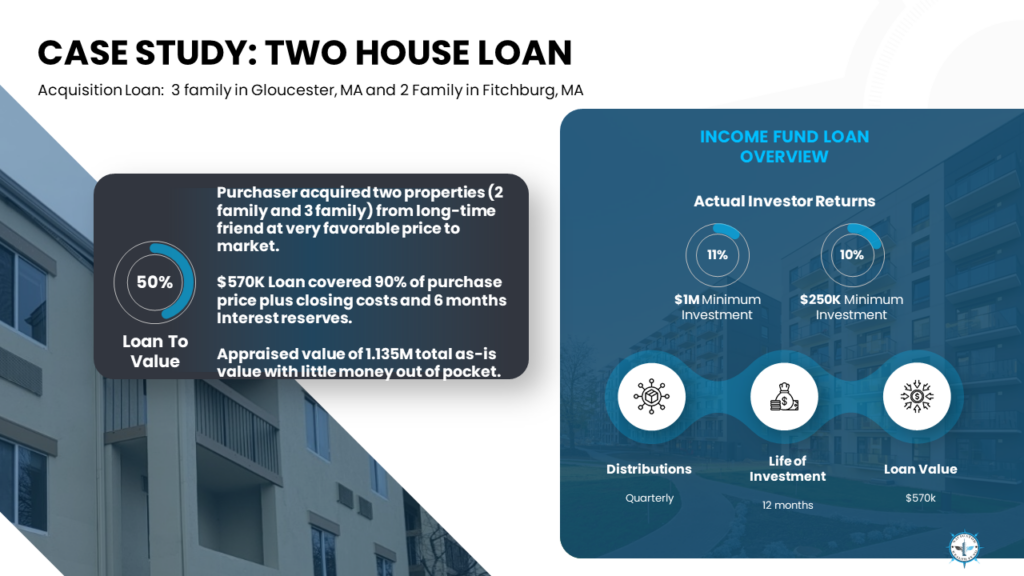

This case study is an example of the second approach. A purchaser acquired two small multifamily properties, a 3-family in Gloucester, MA and a 2-family in Fitchburg, MA, from a long-time friend at a purchase price that was very favorable relative to market value.

Instead of pushing leverage higher, the structure emphasized collateral coverage and cushion from day one.

- Assets: 3-family (Gloucester, MA) and 2-family (Fitchburg, MA)

- Loan type: Acquisition loan secured by two properties

- Loan amount: $570,000

- Loan-to-value (LTV): 50%

- Appraised as-is value (combined): $1,135,000

- Notable structure detail: Loan covered approximately 90% of purchase price, plus closing costs, and six months of interest reserves

Why the starting valuation matters

At a 50% LTV, the loan sits meaningfully below the combined as-is appraised value. That does not eliminate risk, values can change and timelines can shift, but it changes the geometry of the transaction.

A larger equity cushion can help support the loan if something goes wrong:

- The market softens

- The exit takes longer than expected

- The borrower needs more time to stabilize operations

- Unexpected costs appear post-close

The key point is that the deal is not reliant on appreciation to work. It begins with a large built-in buffer.

Two properties as collateral changes the conversation

Loans tied to multiple properties are underwritten differently than single-address loans. The focus shifts to combined support and downside resilience:

- Combined as-is valuation and overall margin

- Collateral condition and liquidity across both properties

- Borrower capacity to carry the loan

- A reasonable repayment plan at maturity

In simple terms, it becomes less about a single asset and more about the strength of the collateral package as a whole.

Why interest reserves matter in real-world lending

This case study also highlights a subtle but important tool: interest reserves.

By including six months of interest reserves in the structure, the loan design acknowledges a real-world truth. Transitions take time. Acquisitions can require stabilization, operational cleanup, or refinancing prep. Reserves can reduce early payment pressure and help keep the project on track, especially when there is a defined plan and timeline.

Reserves do not remove risk, but they can reduce avoidable stress on execution.

The investor takeaway

This case study is a strong illustration of what disciplined short-duration lending can look like when the purchase basis is favorable and the structure begins with margin.

It is not a promise that every deal behaves the same way. It is a window into how loan design can prioritize:

- Collateral coverage

- Downside buffer

- Clear repayment logic

- Structures that match real timing constraints

Learn more

If you want a practical primer on how hard money and bridge loans are typically structured, including why LTV and collateral position matter, start here: https://navwf.com/hardmoneyadvantage

Disclosure

This case study is provided for educational purposes only and is not an offer to sell or a solicitation to buy any securities. Any offering is made only through confidential offering materials and related documents and is available only to eligible investors. Investing involves risk, including the possible loss of capital. Navigator Wealth Fund offerings are not bank deposits and are not insured by the FDIC or any other government agency.