Fix and flip investors do not just need capital. They need capital that matches how a real project unfolds.

A flip is rarely one clean wire and done. It is purchase, then renovation, then timeline management, then sale. That is why many fix and flip loans are structured to support two realities: speed to acquire the property and controlled access to rehab funds as the work gets completed.

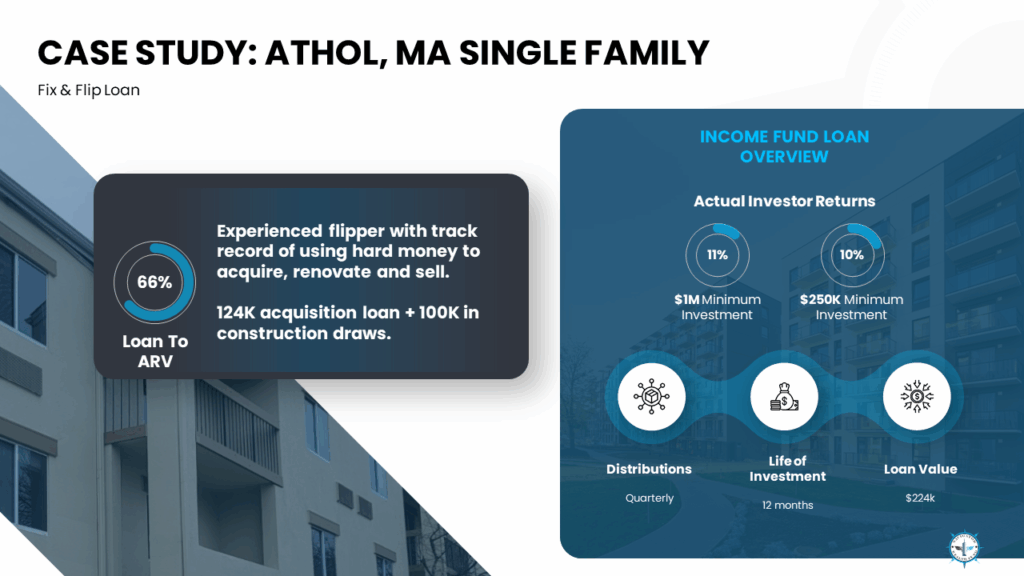

This Athol, Massachusetts single-family case study is a straightforward example of that structure.

- Asset: Single-family property (Athol, MA)

- Loan type: Fix and flip loan

- Loan to ARV: 66%

- Acquisition loan: $124,000

- Construction draws: $100,000

- Total project financing: $224,000

- Borrower profile: Experienced flipper with a track record of using hard money to acquire, renovate, and sell

Why this structure matters in a rehab project

One misconception about fix and flip lending is that the loan is primarily about the purchase. In reality, the rehab phase is where the most execution risk lives.

That is why construction draws exist.

Rather than funding the full renovation budget at closing, draws are released in stages as the project progresses. This structure helps keep the borrower aligned with the plan and helps prevent the project from being overfunded early.

In this case, the structure paired a $124,000 acquisition loan with $100,000 in construction draws, which aligns the financing with how renovation work actually happens in the field.

Why loan to ARV is a key metric in fix and flip lending

Traditional Loan To Value (LTV) focuses on current value. Fix and flip underwriting also looks at ARV, the after-repair value, because the end goal is a resale.

Loan to ARV is a practical lens because it evaluates the financing against the expected end state of the project. It helps answer a simple question: once the improvements are complete, is there still meaningful cushion in the deal?

At 66% loan to After Rehab Value (ARV), the structure begins with room for normal project friction. That does not remove risk, but it creates space for common variables like timeline delays, budget surprises, and shifting buyer demand.

What investors can take from this case study

This Athol loan is useful as an educational example because it highlights three core principles of fix and flip lending:

- Speed has value. Fast closings can be what wins the deal.

- Draws support discipline. The structure matches the renovation timeline, not just the purchase.

- Loan to ARV frames the end goal. It helps investors think about the deal in terms of the completed resale plan, not only today’s value.

Learn more

Explore the Income Fund: https://navwf.com/income

Deep dive framework (The Hard Money Advantage eBook): https://navwf.com/hardmoneyadvantage

Disclosure

This case study is provided for educational purposes only and is not an offer to sell or a solicitation to buy any securities. Any offering is made only through confidential offering materials and related documents and is available only to eligible investors. Investing involves risk, including the possible loss of capital. Navigator Wealth Fund offerings are not bank deposits and are not insured by the FDIC or any other government agency.