Speed is expensive in real estate, and it is usually expensive for a reason.

When a buyer needs to close quickly, traditional financing timelines do not always cooperate. Even experienced borrowers can run into timing friction, including seller deadlines, underwriting queues, appraisal lead times, and lender conditions that do not match the pace of the deal.

That is where short-term private lending often fits. Not as a last resort, but as a bridge. It is a tool designed to help someone move fast today and refinance into longer-term capital tomorrow.

This Lawrence, Massachusetts multifamily case study is a clear example of that dynamic.

-

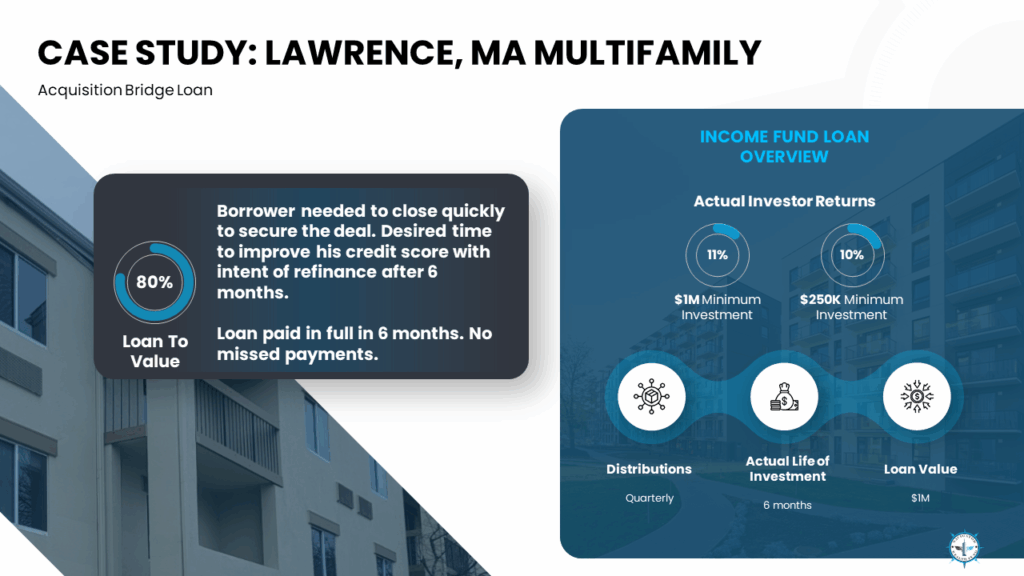

- Asset: Multifamily property (Lawrence, MA)

-

- Loan type: Acquisition bridge loan

-

- Loan amount: $1,000,000

-

- Loan-to-value (LTV): 80%

-

- Actual loan duration: Approximately 6 months

-

- Outcome: Paid back in full (no missed payments)

Why this borrower used a bridge loan

The borrower needed to close quickly to secure the purchase, and the plan was not to keep bridge financing long-term.

The intent was straightforward: use short-term capital to acquire the asset, improve borrower readiness (including credit profile), then refinance after the bridge period.

That exit plan matters, because in private credit a loan is rarely the long-term plan. The typical underwriting view includes:

-

- What is the collateral worth today?

-

- What cushion exists between the loan balance and collateral value?

-

- How does the borrower reasonably repay the loan? (Refinance, sale, stabilization)

In this deal, the repayment plan showed up in the outcome. The loan was paid off in full in roughly six months, aligned with the borrower’s original intent.

Why LTV is often a first-look metric

If you are trying to understand risk in a real-estate-backed loan, LTV is one of the fastest single metrics available.

An 80% LTV structure means the loan sits below the full property value, with borrower equity above it. That is not a guarantee of anything. Markets move, values change, and execution can break. LTV simply frames the starting point.

Navigator Income Fund materials describe an underwriting approach that is focused on short duration and real estate collateral. Within that framework, a bridge loan can sometimes carry a higher LTV than other structures when the rest of the diligence and repayment plan support the deal.

What a clean payoff teaches (beyond the headline)

A payoff is simple on paper: principal returned, interest paid according to the note.

The bigger lesson is why loans like this can exist in the first place. Borrowers are often paying for three things that banks struggle to deliver quickly:

-

- Speed (shorter time to close)

-

- Flexibility (situational underwriting, real-world timelines)

-

- Execution alignment (a bridge that matches a refinance plan)

When those three match the borrower’s true constraint, time, the loan can behave exactly how it was designed to behave: short duration, paid off when the exit plan completes.

Where this fits in an income-focused mindset

For accredited investors exploring private credit, case studies like Lawrence are useful because they make the strategy tangible:

-

- Real collateral

-

- Real structure

-

- Real borrower needs

-

- Real repayment outcomes

Navigator describes the Income Fund as built around short-term, real-estate-collateralized lending, with scheduled quarterly interest distributions (with reinvestment options), and loans that are typically 12 months or less.

That is the bigger picture. It is not betting on one deal, it is building a repeatable portfolio approach where structure, diligence, and duration are intentional.

Learn more

Explore the Income Fund: https://navwf.com/income

Deep dive framework (The Hard Money Advantage eBook): https://navwf.com/hardmoneyadvantage

Disclosure

This case study is provided for educational purposes only and is not an offer to sell or a solicitation to buy any securities. Any offering is made only through confidential offering materials and related documents and is available only to eligible investors. Investing involves risk, including the possible loss of capital. Navigator Wealth Fund offerings are not bank deposits and are not insured by the FDIC or any other government agency.