Not every real estate loan is tied to renovations, construction, or a value-add business plan.

Sometimes the need is simpler and more urgent. A family faces a time-sensitive transition, where real estate equity exists but liquidity does not.

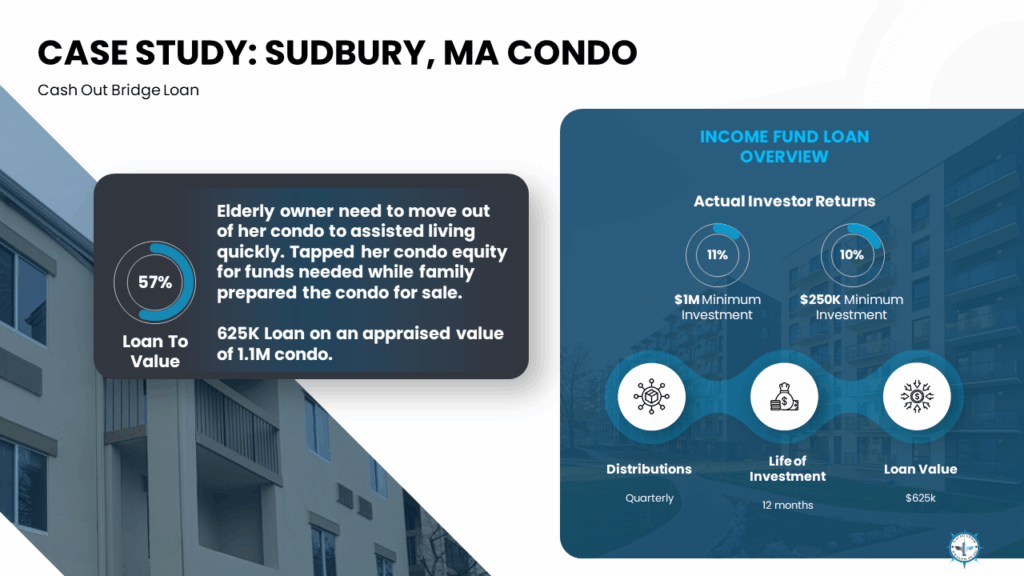

This Sudbury, Massachusetts condo case study, closed in early January 2026, shows how short-term private lending can be used to access funds quickly while a family prepares a property for sale.

Deal Snapshot

- Asset: Condo (Sudbury, MA)

- Loan type: Cash-out bridge loan

- Closing timing: Early January 2026

- Loan amount: $625,000

- Appraised value: $1,100,000

- Loan-to-value (LTV): 57%

- Loan term: 12 months

The real story is liquidity timing

The owner needed to move to assisted living quickly. The family used the condo’s equity to access funds while the home was being prepared for sale.

That is the essence of a bridge loan. It is not meant to be permanent financing. It bridges two states:

- State A: Equity exists, but cash is needed now

- State B: A sale or refinance restores liquidity and repays the loan

From an investor education standpoint, this is a helpful reminder that private credit is not only about projects. It is also about timing, and timing is often the scarcest resource in real estate.

What 57% LTV signals (without oversimplifying it)

At 57% LTV, the loan balance sits meaningfully below the appraised value of the condo.

That does not eliminate risk. Values can change, timelines can extend, and unforeseen issues can arise. Still, the structure reflects a core private credit principle: begin with cushion, then apply diligence and controls to reduce avoidable surprises.

Navigator’s Income Fund framework emphasizes short duration, real estate collateral, and third-party diligence such as appraisals and inspections. Sudbury fits that profile: defined collateral, clear purpose, and an expected takeout event through sale.

Why this kind of loan matters to income-focused investors

Many investors become interested in private credit for one reason: they want a portfolio that is not entirely dependent on public market timing.

Navigator’s Freedom Formula messaging speaks to that mindset, building an income engine, thinking in terms of structure, and reducing the stress that comes from relying on a single outcome.

Case studies like Sudbury make the concept concrete. A loan tied to a specific property, with a defined purpose and term, and interest that is contractually owed by the borrower under the note (subject to borrower performance and fund terms).

The right way to read case studies

A case study is not a promise. It is a window into:

- What kinds of borrower situations appear in the pipeline

- What structures the manager is willing to originate

- What underwriting profile fits the fund’s design

If you are evaluating a private credit strategy, that is the point. Not “will every deal look like this,” but “does the approach reflect the discipline I want behind my income plan?”

Learn more

Explore the Income Fund: https://navwf.com/income

Deep dive framework (The Hard Money Advantage eBook): https://navwf.com/hardmoneyadvantage

Disclosure

This case study is provided for educational purposes only and is not an offer to sell or a solicitation to buy any securities. Any offering is made only through confidential offering materials and related documents and is available only to eligible investors. Investing involves risk, including the possible loss of capital. Navigator Wealth Fund offerings are not bank deposits and are not insured by the FDIC or any other government agency.